In my last post, I wrote a review of GnuCash. Today I’d like to explain some things I’ve learned to track using this financial software.

Reconciling

When I receive a new statement, I first save the PDF to my hard drive. (Hard drive encryption mitigates some of the risk of having all those statements sitting on your hard drive.) Then I reconcile that particular account.

Adjustment account

The adjustment account is an expense account used to keep cash assets accurate. Cash transactions are hard to track, and sometimes my amount of cash on hand does not match the amount recorded in GnuCash. I periodically record this difference as an “Adjustment” expense.

Tax withholding

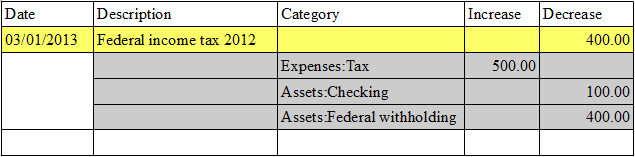

In the US, taxes get withheld from paychecks throughout the year. This tax withholding can be tracked in GnuCash. Each time you receive a pay check (or pay stub), create a split transaction. The gross wage is entered as income. This income will be split between several assets: some income goes to the tax withholding asset, and some income goes to the checking account (net pay).

When it comes time to pay taxes, the money in your tax withholding asset is used to pay your taxes. The taxes actually paid are an expense. There are two scenarios, and each can be covered by a split transaction:

- Your taxes are less than the amount withheld.

- Your taxes are more than the amount withheld.

Here’s an example for situation number 1:

Multiple currencies

Peter Selinger has an excellent discussion of some of the general challenges of multiple currency accounting. The crux of the matter is: Under File-> Properties, go to the Accounts tab, and check “Use Trading Accounts.” This feature doesn’t have a lot of documentation, but it gets the job done.

Reimbursements

When you spend money on a reimbursable expense, you aren’t really spending your own money. You are eventually going to receive that money back, so to you it is an asset. (Not a very liquid asset.) See GnuCash Guide: Chapter 16.

Salary advance

When you receive a salary advance, you receive money you technically haven’t earned yet. This is a liability. You enter the salary advance as a credit to the checking account and a debit to the liability account. When future paychecks come that are reduced (because the company is using them to pay down your salary advance), you can also track this. Enter the paycheck as income, but instead of crediting your checking account, credit the salary advance liability.

Reimbursement advance

A reimbursement advance is money your company gives you to spend for a specific purpose. If you don’t spend it for that purpose, they will eventually need to make you pay that money, e.g. by lowering later paychecks. When you receive a reimbursement advance, you debit that liability and credit your checking account. You continue to record reimbursements by debiting one of your liquid assets and crediting the reimbursement asset. When you submit a reimbursement to clear the advance, you debit the reimbursement asset and credit the reimbursement liability instead of your checking account.